Loan providers utilize this are accountable to see whether or perhaps not a borrower is likely so you can default to the a home loan

To make use of the step three.5 % minimal downpayment choice, you truly need to have a beneficial FICO score zero below 580.

Your credit score are lots one is short for your creditworthiness so you can lenders who happen to be deciding whether to grant you that loan.

Your debt proportion reveals your much time-name and you can small-label financial obligation given that a percentage of the overall property. The lower the debt-ratio how many installment loans can you have in Vermont, the better the possibility try from qualifying to own a home loan.

When you look at the mortgage purchase techniques, you’re provided revelation documents that provides additional facts about the house financing agreement.

Credit ratings are definitely the really widely accepted fico scores

Disregard products are believed a variety of prepaid service attract on your own financial. These types of “points” is actually a portion of your own loan paid-up front that thus lowers the fresh mortgage’s rate of interest.

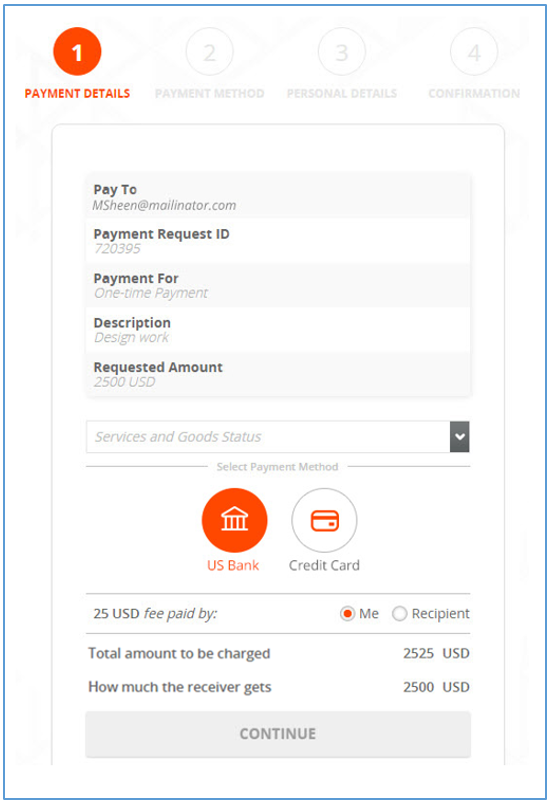

The newest advance payment on the home is extent you only pay the lending company upfront in order to keep the loan. The amount varies centered on what you can afford, and mortgage conditions one to vary according to the financial.

A major difficulty somebody deal with of trying to purchase a property is actually saving right up towards the downpayment. To simply help overcome this dilemma, there are down-payment direction applications that give homeowners that have has that go into the fresh beforehand and you will settlement costs.

You have to pay the serious money put once your render for sale could have been recognized because of the vendor, to show your committed to buying the household.

Being entitled to an enthusiastic the latest FHA financial or a keen FHA re-finance, there are certain requirements you will have to see because the a debtor. When it comes to an excellent borrower’s qualification, new FHA financing system also offers a lot of self-reliance.

Home guarantee is the number of ownership you have on the family. The collateral on your own domestic develops since you make money, as you very own a lot more of it.

Their escrow account is established by your financial under control to get financing that go towards expenses possessions taxes and household insurance rates.

The fresh Government Property Management, or even the FHA, was a federal government-work with department that provides insurance rates with the FHA-acknowledged mortgages, to boost reasonable construction regarding You.S.

The FHA kits borrowing from the bank criteria you need to fulfill if you are to qualify for a federal government-backed home loan

FHA capital costs include the insurance fees required to support the financing. Extent you only pay for the so it insurance rates relies on the size of one’s financing, its identity, together with advance payment you made.

FHA mortgage brokers has a couple of regulations and you can direction and therefore performing lenders have to realize to ensure that money to be insured by the United states authorities. These types of laws are built-up in one single resource book named HUD 4000.step 1.

The newest FHA has established limitations toward matter it does insure to your government-backed financing. These limits will vary based on items instance location, particular possessions, and you may parameters getting traditional funds.

FHA money is actually insured by government to let help the supply of affordable homes from the U.S. These fund is supported by new FHA, and that protects loan providers out of significant loss.

HUD necessitates that any house becoming financed which have a keen FHA mortgage matches the latest FHA’s Minimum Requirements. To make certain that financing to be offered, the house should be considered safe, safer, and sound.

You’ve got the choice to re-finance your residence through the exact same otherwise a separate lender, so you’re able to alter your latest financial with a brand new you to definitely that offers all the way down interest levels, or to borrow money facing your residence’s security.